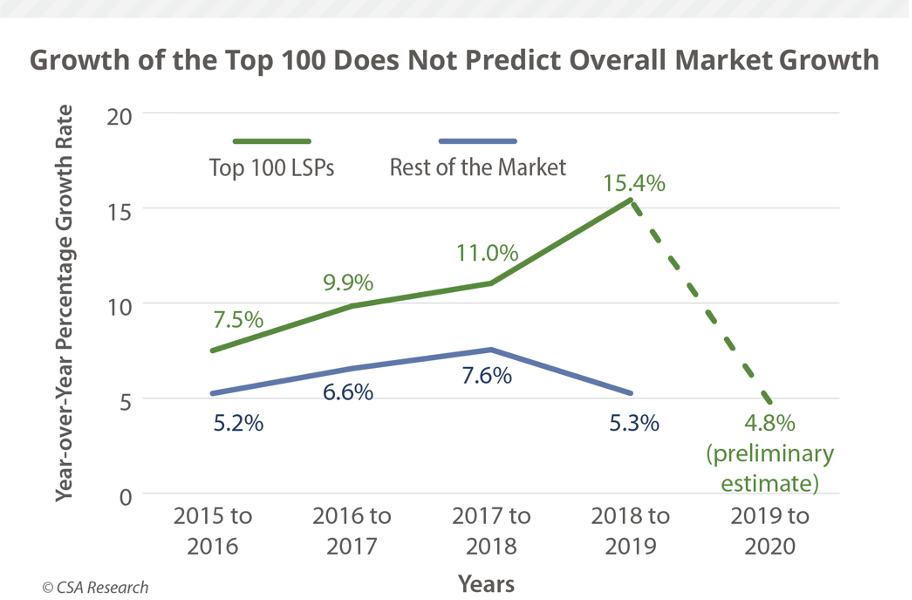

It is unwise to statistically extrapolate the entire market from the Top 100 LSPs or even the Top 193 LSPs (CSA Research's ranking of the top 100 LSPs globally plus the top regional LSPs).

Since 2015, the Top 100 LSPs have grown an average of 83% faster than the rest of the market. The poor correlation between how the Top 100 LSPs or the Top 193 LSPs and the rest of the market have grown makes it impossible to generalize from one segment to the remainder.

This is particularly true of the last year (March 2020 - March 2021). Data in the report shows that smaller LSPs experienced significantly greater volatility during the COVID-19 pandemic.